With the announcement of INR 20 lakh core stimulus package to combat Covid-19 lead economic crisis, the buzz of demand creates supply or supply creates demand, once again knocking the window of intellectual battle.

The enigma of supply creates demands is the brainchild of classical economists J.B Says which later on challenged by Keynes and proposed & proved a reverse order hypothesis. The magnitude of this battle gets more intensified with the release of fourth-quarter data of the financial year 2020 (Q4FY20) by CSO (Central Statistical Organisation) on 29th May in the previous month.

The Q4 GDP growth rate data paints a very pitiful picture of 3.1%, which is the lowest since the GDP base year was revised to 2011-12. Interestingly, the data hardly include the impact of a week lock down- as lock down 1.0 stared from 25th March.

At this moment the overall growth rate in FY20 has been historically low and does not deserve any sense appreciation at any fronts. Be it statistically, politically, mathematically, and academically (including policy making). Its outcome is quite visible in the recently revealed Moody’s historically downgrading of India’s sovereign rating from Baa2 to Baa3- the lowest investment grade.

Covid-19 Lead Economic Crisis

For the last four months, the whole world is witnessing the most significant attack on humanity at a time when the advancement and the supremacy of science and technology are the most pressing subjects for countries to illustrate their dominance and power.

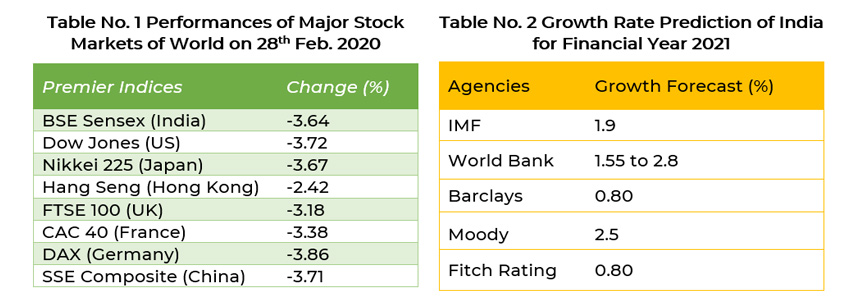

The complete choking of the health care system of even the most advanced and nations having the global best health care facilities is the typical example of the mockery of scientific advancement and the invincibility of COVID-19. The powerful invincibility of this virus has completely uprooted existing systems of economic and non-economic activities in the majority of the countries across the world (see table no 1).  So is the case with India (see table no. 2)

So is the case with India (see table no. 2)

India’s industrial output contracted unprecedented 16.7% in March and is bound to fall more in April as well, as the whole country was under complete lock down for the entire month. Core sector output falls 38% in April and Steel & Cement output is falling by more than 80% YOY.

The non-availability of any scientifically approved medicine and the nature of exponential growth of spreading of COVID-19, has forced the governments and concerned authorities to weaponise the physical distancing among people via shutdown the entire country to combat over it.

Unquestionably, it has an enormous adverse impact on the economy and lives and livelihood of the people. Specially the lower middle class, including the daily wage workers and migrants’ labours have been the centre of plights aroused from entire shutdown. Recently the news related to the pathetic state of being a migrant labourer has been evident enough to believe so.

Measures By the GoI (Government of India)

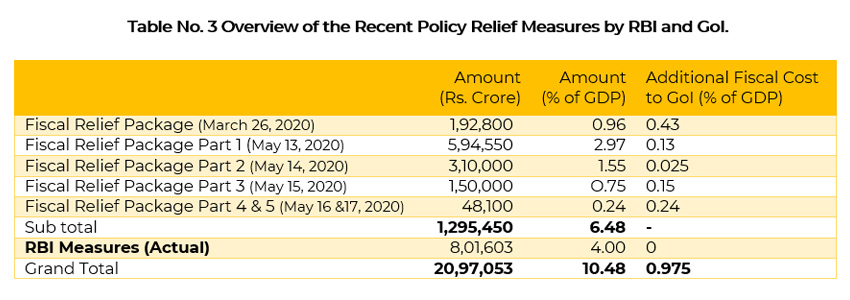

Whether to go with ‘physical distancing’ to save people’s life or to ‘protect the livelihoods of 800 million lower middle class- was the toughest choice. The GoI (Government of India) and RBI (Reserve Bank of India) has smartly overcome from this enigma by announcing the relief package of INR 20 lakh crore (see table no. 3) and easing the protocol of lock down in the phased manner. Note:In absolute terms the total Central Government’s Fiscal Cost amount to Rs. 2,17,095 which 1.085% of GDP

Note:In absolute terms the total Central Government’s Fiscal Cost amount to Rs. 2,17,095 which 1.085% of GDP

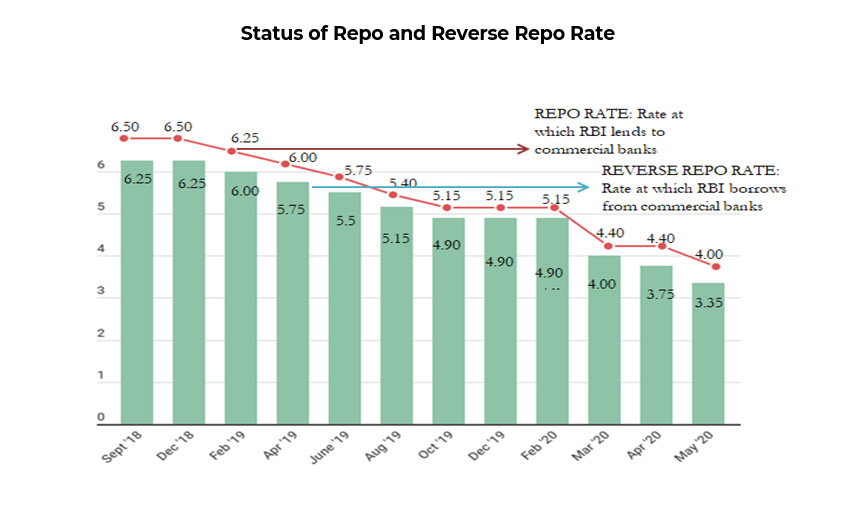

Apart from these, RBI has made a series of announcements to boost liquidity in the economy. Repo rate has reduced to the historical 15 years low to 4.0; CRR cut to 3%- first time since January 2013. Reverse repo rate has also historically reduced to 3.5% ( see figure no. 1). Three month moratorium of all kinds of retail loan payments was also in the basket of a series of announcements.

Therefore, the ploy used to tackle the issues such as- (a) PDS (Public distribution system) for the distribution of food grains; (b) Social security pension and cash transfer (c) Reforms like; new definition of MSMEs, the new policy for PSUs, higher FDI in defence production, (d) Infrastructure push through affordable rental housing for migrants, agri infrastructure fund, the extension of middle-income housing scheme (e) Helping stress business through relaxation in insolvency law, liquidity support/refunds and funds for stressed NBFCs and (f) Boosting liquidity via CRR, SLR, Repo & Reverse Repo rate, collateral-free loans/equity for small business, Rs. 2.3 lakh crore extra credit to farmers and special liquidity and partial guarantee for NBFCs.

The rational of this announcement depends on the ideas of demand & supply up to a large extend. The success of these announcements actually depends on whether supply will follow its demand or not. If not, then the notion of demand creates supply will again be proved plausibly logical.

Seeing the measures taken so far, it has more for supply and less in demand. Although private consumption expenditure is very crucial as it constitutes close to 60% of GDP.

The ongoing status quo is not conducive for V shape recovery of the economy. The consumer sentiment is down because of job losses/ pay cuts across classes. Having such backdrop, it becomes quite imperative and practically sounds to take measures that can spur demand in the economy. Boosting consumer sentiment is one of the best tactics to do so.

But unfortunately, the whole stimulus package lacks on the demand side. As the whole sets of announcements did not address the measures that can speed up recovery. Such measures could be likes: tax cut; lower GST on consumer goods; much for the middle class; policy to directly boost job creation; more direct relief for low income unemployed; incentives for housing and auto and many more. Therefore, it appears that policymakers would have thought to revive the economy through the supply side. It’s quite interesting to see, how the Indian economy reacts towards these stimuli.

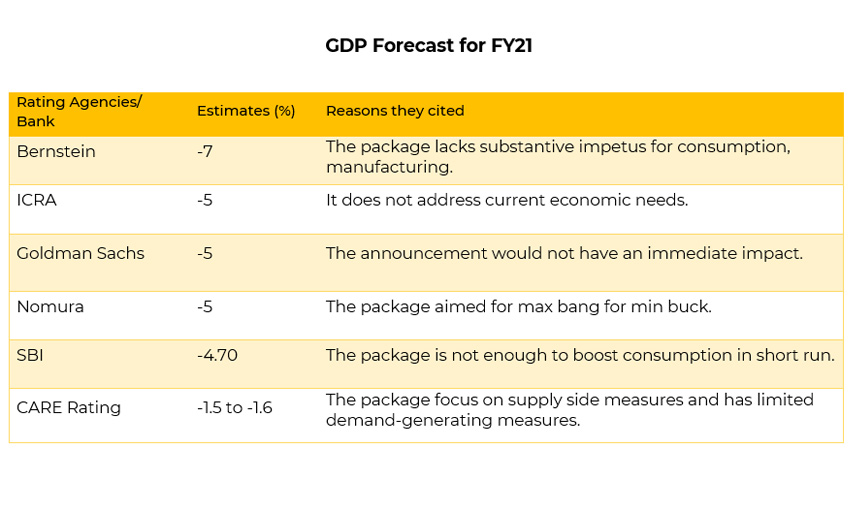

Reaction of Rating Agencies

Days After Stimulus Package of INR 20 lakh crore, the rating agencies and banks have further reduced their assessment of India’s GDP growth for FY 21.

What ever so far is done to address the lives and livelihoods of people, deserves a satisfactory sense of appreciation as of now. However, at the same time, whether this relief package and their ways of delivery are sufficient enough to address the current status quo of the economy and the pathetic state of being of especially poor and migrant labourers or not? It is such a question that still remains to be answered. Seeing the unavailability of actual data and high skewness in social, financial and economic inclusion of actual poor, it’s not appropriate to comment at this point. But sensing the gravity of the new world disorder because of Covid-19 and tension between US and China, it’s not inappropriate to focus on supply side measure to clutch the long-term growth and future opportunities.

Covid-19 and New World Disorder

The GoI made this announcement at a time when the world is on the verge of new disorder. Out of this Covid-19 a new kind of narratives has emerged against China across the world. China- the world’s manufacturing powerhouse and the world’s largest exporter and second largest importer of goods; is being accused for hiding Covid-19 data.

As a result of it, anti-globalisation sentiments like protectionism, nativism, and trade & ideological war between China and US are gaining its momentum. The imposition of tariffs by the US and retaliation by China on billions dollars worth of goods is the typical illustration of anti-globalisation.

As a consequence of new narratives, hundreds of MNCs (Multinational Corporations) are looking for changing their production base from China to some other business conducive countries.

India’s Prospect

Sensing the gravity of new opportunities, India is preparing herself firmly to clutches all such opportunities. Seeing past and current policies, it appears that the GoI is looking for long term perspective and gradually setting the pedestal for the world’s largest manufacturing hub. Preferring supply side measures overs demand side is one such indicator.

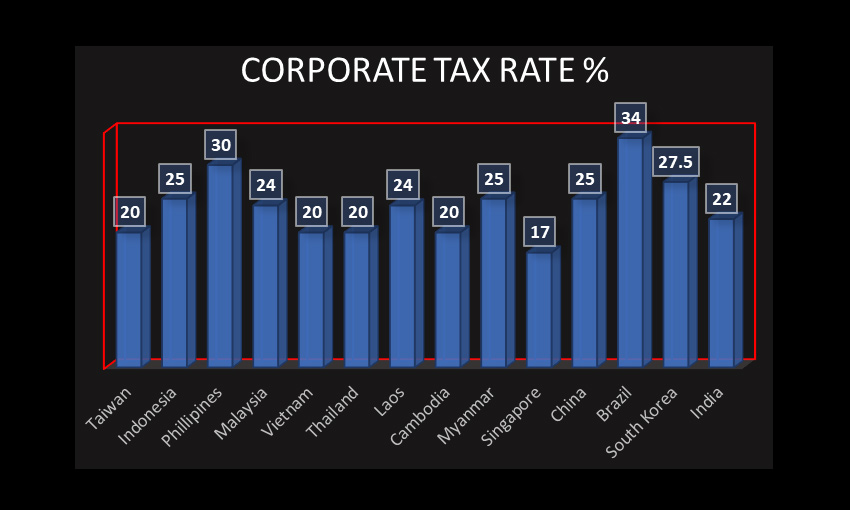

During the month of September last year, Finance Minister (FM) announced a reduction in corporate tax rate from 30 per cent to 22 per cent. The effective tax rate (including 10 percent surcharge and 4 percent cess) reduced from 30.9-34.61 per cent (up to Rs.1Cr. 30.90%; between Rs.1 to10Cr. 33.06%; and exceeding Rs.10Cr. 34.61%) to 25.17 per cent.

For new manufacturing units set up after 1st Oct. 2019 and commencing operation by 31st March 2023 the effective tax rate announced to reduce to 17.01 per cent from 29.10 per cent earlier. Minimum Alternative Rate (MAT) is lowered to 15 percent from 18.50 percent for companies availing the facilities of exemption and incentives.

The reduced tax rate positioned India at the most competitive position among her competing peer see figure. no. 2.

India is having the best demographic dividend together with a competing tax rate and a good sum of INR 20 lakh crore stimulus packages, seems to provide the attractive and favourable spot for prospective investors. Till now Vietnam, Taiwan and Thailand have been getting the benefits of new narratives. Now India is in the best position to grasp all kind opportunities.

Thus focusing supply side and firmly riding on it to secure long-term Investment are not unquestionable. But for immediate recovery of the economy requires short term injection to spur demand and stimulates the virtuous cycle, which is the need of the hours for Indian economy.