The (COVID-19) bell is tolling As COVID-19 wreaks its havoc, the end of John Donne’s poem ‘No man is an island’ (cited in the previous edition of Economic Insights) seems unhappily ever more appropriate. Alas, the bell really is tolling for all of us! Too many deaths, businesses going bust and jobs being lost. With so much human misery it seems tactless to write about financial markets. However, as a result of necessarily draconian government interventions, COVID-19 has been rapidly transformed from a catalyst for a stock market correction into seismic economic shock waves.

The (COVID-19) bell is tolling As COVID-19 wreaks its havoc, the end of John Donne’s poem ‘No man is an island’ (cited in the previous edition of Economic Insights) seems unhappily ever more appropriate. Alas, the bell really is tolling for all of us! Too many deaths, businesses going bust and jobs being lost. With so much human misery it seems tactless to write about financial markets. However, as a result of necessarily draconian government interventions, COVID-19 has been rapidly transformed from a catalyst for a stock market correction into seismic economic shock waves.

The first shock was to international trade and supply chains, which although potentially recoverable, was already set to become another brake on the global economy, hitting China hardest. This is now being overtaken by the first wave of what will surely be several demand shocks as a result of the ‘lockdowns’ imposed in response to the unprecedentedly high levels of contagiousness and shortage of medical staff, beds and ventilators needed for sufferers. The reduction in economic activity is already vividly illustrated by the reduction in air pollution in China and Europe (Figure 1).

Figure 2 They need more than a dime, buddy!

Cash for Demand

In the grim terminology of epidemiologists, ‘suppression’ involves deliberately slashing economic

activity. Economists are having a field day in competing with ever gloomier forecasts but it seems

clear that China will have experienced a deep recession in Q1 and then a better but still poor Q2,

with the advanced economies (i.e. China’s customers) following a few months behind and some sort

of recovery underway by the end of the year. In order to mitigate the first shocks China has chosen a

more conventional path of public investment and boosting funding for small businesses while, with

commendable urgency, advanced economies are taking more drastic action. The richer the economy

the higher proportion of GDP is accounted for by Consumption (nearly 70% in the US) and by jobs in

the Service Sector. Accordingly, simply leaving workers to take their chances in lockdown would

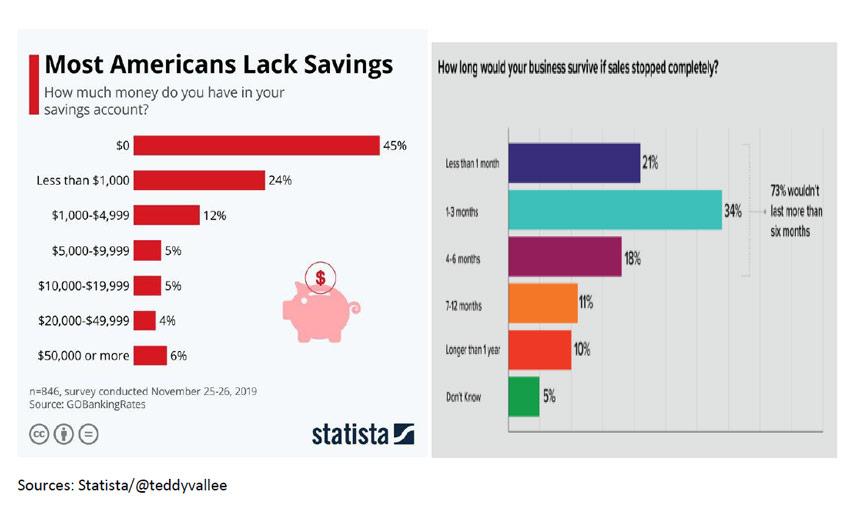

result in a collapse in Demand. Survey data from the US (Figure 2) shows that over 80% of Americans

have savings of less than $5,000 (in the UK around 50% have less than £1,500) and 20% of American

business would not survive more than one month without sales (50% not more than 3 months). To

put it crudely, people and businesses need cash and fast.

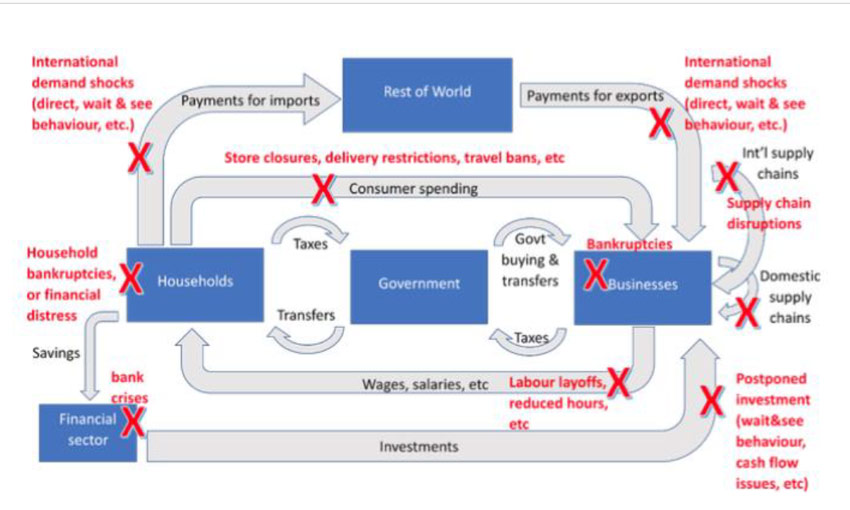

Figure 3 Plumbing a modern economy (simplified)

The plumbing of modern economies is complex but Geneva-based Professor Richard Baldwin has

designed a model (Figure 3), which although simplified, shows where the crucial blockages, burst

pipes and feedback loops are most likely to occur. Households and businesses really are symbiotic

and any rupture really does requires government intervention to repair it and, in extreme

circumstances, such as those currently, to restart the flow. Banks are essential both as conduits of

and contributors to flows in the form of credit. Investors, ‘Rest of the World’ importers and exports

are also important contributors.

Unlike their plight in 2008, most banks are not badly or immediately exposed to a collapse in

Demand, although nor can they meet all the inevitable funding requests from their customers.

Some, especially in Europe, must be dreading another cascade of non-performing loans. Hence, the

plans for guarantees of emergency bank loans and extra liquidity from the central banks as

governments in different countries frantically work out how much cash needs to be made available,

how to get it to where it is most needed and when. Also to be settled are important details such as

the balance between companies and workers, tax breaks or straight handouts, relief for the selfemployed,

equity stakes in strategic companies and restrictions on buybacks. Most governments,

with some notable Anglosphere exceptions, are doing quite well so far in buying time for their health

services to cope somehow. Nevertheless, unless they can get people back to work within 2-3 months

the amount of cash required will start to compound and it may already be too late to save some

businesses in the travel, hotel, restaurant, sports and non-food retail sectors. Funding is another

issue but it seems most governments (including Germany!) are preparing to borrow up to 10% of

GDP and expect the central banks to step up to help too.