Despite the efforts of all the medical and scientific experts, much remains to be discovered about COVID-19. It is not life-threatening to most of us and yet highly contagious, with dire consequences for those it does attack. The best way of containing it is proving to be social distancing even without a complete lockdown (as in Japan) and this seems also to be the case in dealing with new outbreaks, such as those in Singapore and South Korea. Lockdowns and travel bans still help even if not imposed immediately as in Italy and Spain. Testing and tracking is already established as the best defence against further potential waves. Building and maintaining trust through decisive actions and clear communication with the public has been the key to successful containment in Asia and much of Europe. The challenges may have been greater for democracies but New Zealand, Germany and the Nordic countries (all liable to subversion on social media by Russia and China cyberbots) have shown how it can be done.

Nevertheless, even successful containment can only limit rather eliminate the economic damage and major exporters such as China, Germany and ASEAN counties will suffer from the mistakes of their trading partners, including those leading laggards the US, UK, India, Brazil and Mexico.

Alastair Winter

Thought Leader,

MarketExpress.in

Global Sharing Platform

Here in the UK, the scientists are clearly at odds with the Government’s haphazard and hazardous approach to easing while hospitals, especially in high infection areas, are preparing for a second wave to start before the end of June. Iran is already reporting a surge in new cases following the lifting of most of its restrictions. The ‘optimists’ are surely right in expecting no new complete lockdown anywhere but with a vaccine still unlikely to be available until next year, if at all, social distancing (self-imposed as well as a mandatory) will continue to disrupt businesses and economies around the world.

Figure 1 once again draws on Professor Richard Balding’s splendid simplified model of an advanced national economy. The key flows are appropriately at the centre, highlighting the symbiotic relationship between Consumer spending and wages from employment. The key is to keep money flowing to households to spend on goods and services provided by business and to help companies hit by lockdown to survive, including retaining employees, until conditions improved. To be fair, in contrast to their vacillation on other measures, the US and UK government came up with admirable speed with a very effective combination of furlough payments to employers, grants to the self-employed and extra benefits to those out of work (Figure 2 dark blue areas). Companies are also being helped by tax holidays and delayed payments (dark orange areas) and also loan guarantees (light orange and blue areas and some of the green areas), which will be less effective if they have to be settled too soon. Equity injections, such as those made in 2008-9, would be better and may yet happen for ‘strategic’ companies. Last week, the hitherto frugal Mrs Merkel came up with a €130bn package that included direct payments, guarantees, skills training and investment in innovative technologies. This is likely to be a blueprint for other governments, even for those that have their own national ‘independent’ central banks with which they are ‘collaborating’ (most of the green areas).

Figure 1 once again draws on Professor Richard Balding’s splendid simplified model of an advanced national economy. The key flows are appropriately at the centre, highlighting the symbiotic relationship between Consumer spending and wages from employment. The key is to keep money flowing to households to spend on goods and services provided by business and to help companies hit by lockdown to survive, including retaining employees, until conditions improved. To be fair, in contrast to their vacillation on other measures, the US and UK government came up with admirable speed with a very effective combination of furlough payments to employers, grants to the self-employed and extra benefits to those out of work (Figure 2 dark blue areas). Companies are also being helped by tax holidays and delayed payments (dark orange areas) and also loan guarantees (light orange and blue areas and some of the green areas), which will be less effective if they have to be settled too soon. Equity injections, such as those made in 2008-9, would be better and may yet happen for ‘strategic’ companies. Last week, the hitherto frugal Mrs Merkel came up with a €130bn package that included direct payments, guarantees, skills training and investment in innovative technologies. This is likely to be a blueprint for other governments, even for those that have their own national ‘independent’ central banks with which they are ‘collaborating’ (most of the green areas).

The other potential blockages in Professor Balding’s model may be less important but they cannot be ignored:

Finance: unlike 2008-9 the major banks do not seem to be short of funds (Figure 6 bottom left) at least not yet, which makes even more important their appetite to carry on lending through a recession, thereby helping to keep funds flowing (bottom right). Defaults and arrears on student and car loans (much of it already securitised) were already a problem before the COVID-19 crisis and now the delinquency rate on mortgages, commercial as well as personal, is rising rapidly as tenants and property owners struggle to meet their obligations. Equity and bond funding from institutions, however, should continue to be available to companies that are able to demonstrate that they can thrive.

Domestic supply chains: (Figure 1 middle right) disruption is likely among suppliers who have cut back capacity too sharply or if their customers have found alternatives. Jobs could be lost and/or wages cut. Any major supply shocks would, of course, be inflationary.

International trade: (Figure 1 top) many of the issues are the same as for domestic supply chains and the model is a timely reminder that very few economies could ever be self-contained, which means that deep recession in most advanced economies will hold back the otherwise promising recovery in Asia, including in China itself. Armed warfare is notoriously the ultimate economic stimulus but despite their sabre-rattling neither the US nor China, thank goodness, seems willing to bear the human and financial costs. Trade wars, at least in the early years, damage economic growth until and unless suitable domestic substitutes for imports become available and viable replacement export customers signed up.

Judging by market movements, the Risk Takers amongst investors are satisfied that enough has been done to result in the proverbial ‘V-shaped’ economic recovery, that COVID-19 will be neutralised and ‘normality’ will return sooner rather than later. This involves so many heroic assumptions that it almost emulates Admiral Nelson’s putting his telescope to his blind eye at the Battle of Copenhagen!

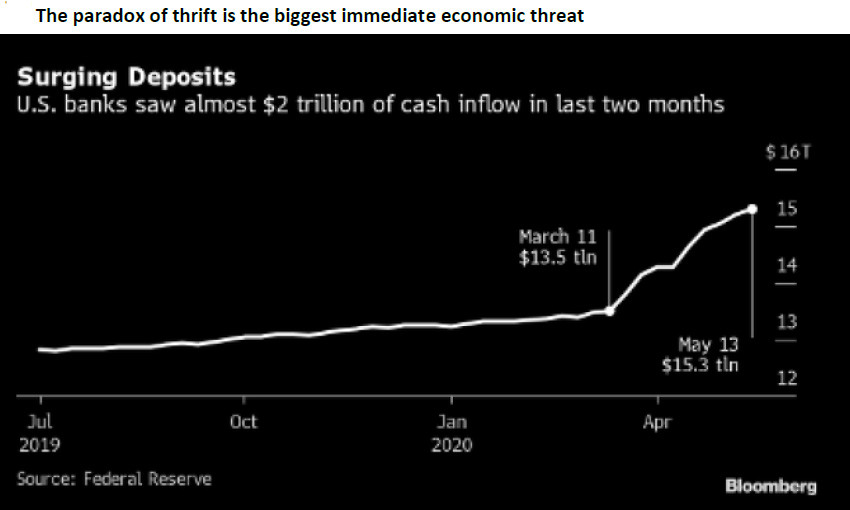

In fact, the biggest immediate threat is not insufficient government support, even though that is also highly likely, but that of consumers’ taking fright, saving rather than borrowing and spending in the way they have done in advanced economies for the last 30 years and more recently in China and other rapidly developing economies. Economists call the resulting constraint on GDP growth ‘the Paradox of Thrift’, a concept often associated with Keynes, who certainly fretted over it, but which was identified long before him.

Figure 3 shows what has been happening in the US since COVID-19 started hitting the headlines. The surge in deposits will include those both from individuals and companies, after many of the latter drew down their committed bank lines and/or issued new bonds to ensure their survival. Consumer credit in both the US and UK reversed abruptly into net repayments in March and plunged further in April. If these trends persist in those and other economies, and Consumer Confidence surveys are not encouraging, then the blockages in the centre of Figure 6 will start to form. No wonder governments everywhere are so concerned!

Looking further ahead makes even more improbable a return to the ‘normality’ of January 2020. COVID-19 unleashed challenges that are shared by most countries, albeit with varying degrees urgency and intensity and which have been building for years. A major increase in structural unemployment is just the start and will raise questions not just on investment in new technologies but also on the purpose and organisation of all stages of education and training. The latter is directly connected to the growing unease with inequality, which in the widest sense is not only unfair but stifles the economic benefits of social mobility. That in turn leads to issues on the provision of social services such as health (including mental health), care of the aged and homelessness. Then there are the global issues of food and water shortages, migration, pollution and climate change. These ‘genies’ will not easily go back in their bottles and governments everywhere will have to find the money to address them. Companies will have to respond more to the evolving attitudes of their customers and employees and moderate the rewards to shareholders and top executives.

GDP will, of course, recover around the world to the levels seen in January, albeit that growth was slowing just about everywhere. The ECB is cautiously predicting this will not happen until 2023 for the Euro Area while China and some ASEAN countries are aiming for as soon as next year. The big increases in public spending should cover in part the inevitable slowdown in Personal Consumption but perhaps the very concept of GDP, or at least its composition, will be replaced with wider measures of ‘wellbeing’. There really is a lot to wish for and even to hope for but this does not realistically include a ‘V-shape’ economic recovery and buoyant corporate revenues. Accordingly, to build up firm expectations of ever more gains in global equities is to risk disappointment and painful losses.