A Historical overview:

In late 1990’s East Asian Crisis created ripples in the global market and it turned out to be a currency crisis, credit crisis and a crisis of confidence, but the impact broadly remained contained to the ‘Asian Tigers’. A decade later, I remember reading a headline saying, ‘US sees 130 bank failures in 2009; six go belly up in a day’, and it formed a major news item in late 2009. The sub-prime crisis turned out to be an account of failure of systems and checks & balances and put the US economy in banking and financial crisis. It was followed by the European debt Crisis of 2011, when the PIIGS failed to generate enough economic growth to make their ability to pay back bondholders the guarantee it was intended to be. What followed was a series of bailouts.

Are such crises new to us? No! Actually, we seem to have entered another cyclical face of crisis kick started by the US-China trade war and overall demand slowdown. On the cost of being little boisterous, it may not be a loud thinking that the world is slowly moving towards another phase of slowdown, whether we see the inversion of yield curve as a precursor of US slowdown or the overall falling growth rates across nations.

The Indian Perspective:

It would be quite hyperbolic if I say that India is unaffected by the ongoing trade war and other geo-political developments. However, saying that everything is down may also be an exaggeration.

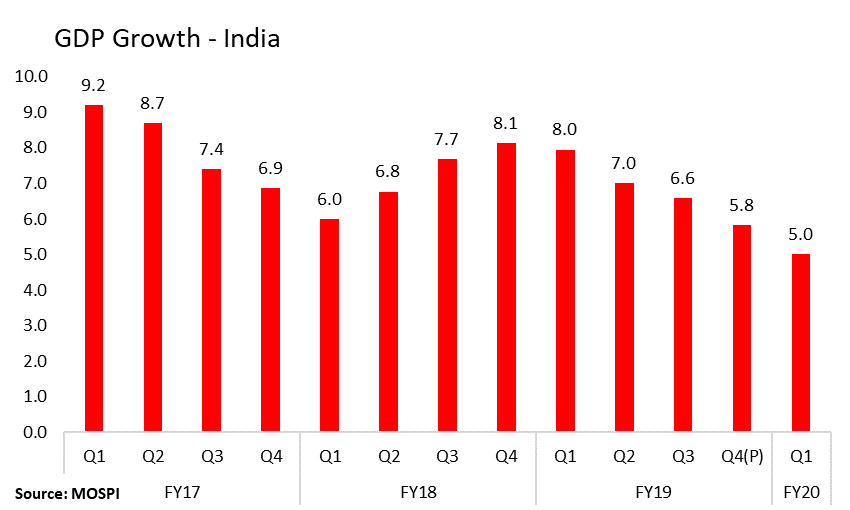

The GDP growth has been falling and it is not a hidden secret. The GDP growth on a quarter on quarter basis has registered a decline and from a peak of 9.2% in Q1 FY17, it has decreased to 5% in Q1 FY20. The slowdown has been quite steep in manufacturing followed by services and agriculture. The manufacturing, which registered a growth of 10.2% in Q1 FY17 has declined to a meagre 0.6% in Q1 FY20.

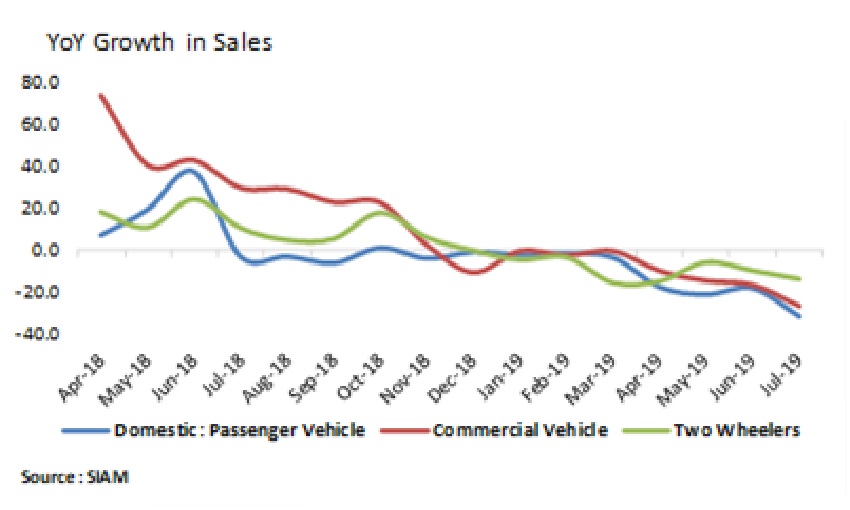

The auto sector is facing its worst ever slowdown in around two decades. The domestic vehicle sales, commercial vehicle as well as the two-wheeler sales have failed to move out of negative growth territory. The falling sales has resulted in production cuts leading to job losses. There is news galore on the thousands of job losses in the automobile and related business segments.

The real estate sector has huge unsold inventory and as per the quarterly report real Insight published by PropTiger.com home sales have declined by 11 per cent in Q1 FY20 in the nine major Indian markets, when compared to a year-ago period. Further, during quarter ending June, new project launches have also reduced by a drastic 47 per cent year-on-year (YoY).

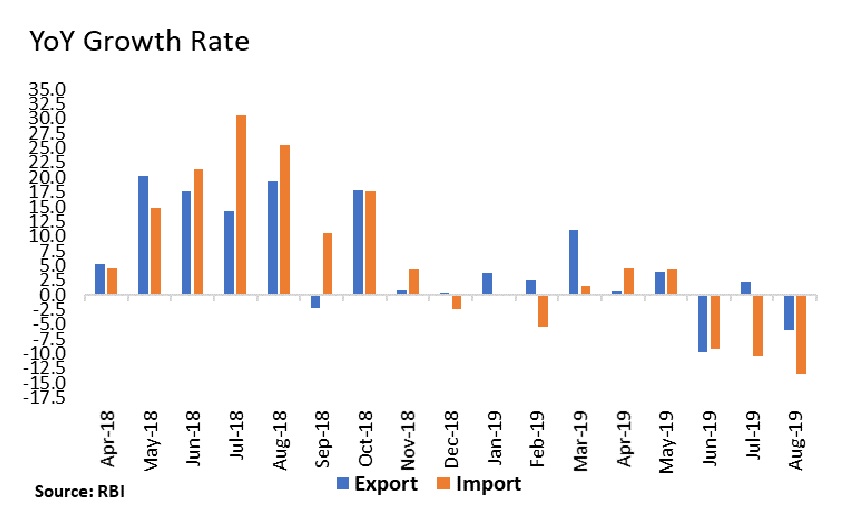

The exports and imports both have been showing signals of weakness. Though the latest exports figures show a marginally positive growth of 2.2 per cent, the high foreign exchange earners such as refinery products, engineering goods and gems and jewellery still reflect a decline. Imports continued to decline.

I would still say that the Indian economy is still showing signs of resilience with the GDP growth rate still registering the second-best growth rate at global level.

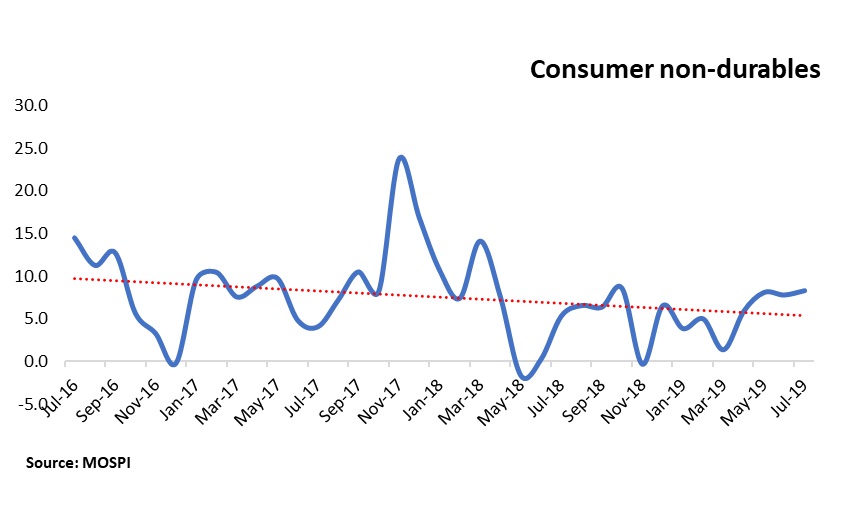

The growth of the Indian economy so far has depended upon the consumption driven growth. The growth in the consumer non-durable segment has, despite of the slowdown, moved in the positive zone. After touching the peak levels in Nov’17 (23%), the consumer non-durable segment growth after bottoming out and post recovery has turned virtually flat.

So, to say that the consumption story is yet not over. Then what could be possible reasons for this slow down and can the rate cuts solve the problem?

Interest Rate Cut: Is it the panacea of all problems:

The rate cut rhetoric and impact in spurring the growth takes us to ‘Keynesian theory’ which articulates that for an economy to grow, the aggregate demand needs to be pushed up. For increasing the demand the policy makers should actively use the tools of fiscal policy. Keynes came out with his theory in 1930’s on the background of the classical thinking that, in case of any depression or slump the market would automatically adjust to equilibrium without government intervention. No economy can survive if the recession continues for a long time. He, therefore, advocated for fiscal support by means of government borrowing to inject money into the system and increase the spending and the consumption levels in the economy. In the present case also, the government shall stimulate the economy by directly spending through public expenditure policies.

No economic theory is born without having fall outs of its own. The increased spending of the government along with other benefits in the form of tax sops often leads to deficit financing which may not give long sustainable results. If a fine balance is not maintained between money injection, increased public expenditure and long-term fiscal prudence it may lead to inflationary pressures leading to an unstable economic situation.

Later Milton Friedman said that the growth rate of the economy or the national output can be influenced by changes in the monetary aggregates or the money supply in the economy.

In India, the regulator has given relief on the monetary front by softening the interest rates. However, the economy has not responded, as desired, to the easing of interest rates which is visible in the credit off take in the system. This may, therefore, call for fiscal stimulus to push up the growth of the economy. The active role of the government does seem to spur demand in the economy which translates into better growth rate of the economy. We have to wait and watch for the impact of this support to take place. At present, there are no boosting signals if we look at the data of the banking industry. The banking industry has not only been experiencing increase in the default levels but there are no takers of credit as well.

This however, signals towards revival of Keynesian principles that it is the direct interference of the government forces which can boost the prospects of the economy by directly targeting the aggregate demand of the system.

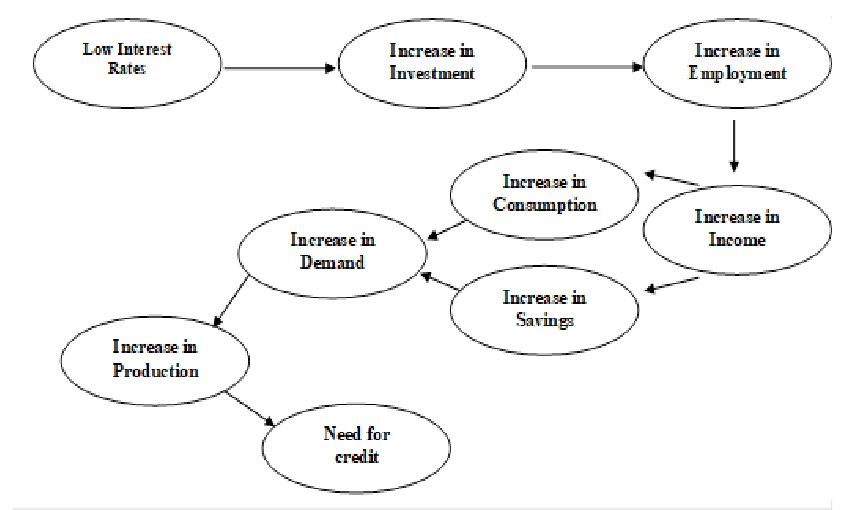

The above chart makes it clear that benign interest rate regime is one of the stimulating measures for the growth rate in the economy under normal conditions since it spins the business cycle in the economy. The only catch in the entire picture is that there is a limit to credit expansion and secondly that for credit to go up, it has be fueled by an equivalent amount of savings and consumption in the economy. What if there is no increase in consumption? Would the demand be there? Certainly not.

Where lies the Solution:

The ultimate end, therefore, is to create demand. Increasing the investment activity in the economy through the banks becomes possible only when there are takers of credit and the investment activity picks up only when there is demand in the economy.

Lowering of interest rates only would not serve the purpose of boosting the growth rate of the economy in the absence of demand in the system. The flowchart given above also makes it amply clear that the economies can grow if investment activity or the consumption levels in the economy increase even when soft interest rates are not able to bring around desired results. It is either from the government, the public sector or the private sector. A concerted effort from the combination of these three would certainly create prospects for an increased demand leading to real growth in the economy.

We can say in the end that, we are living in a complex world of finance and growth, where everything is interrelated, integrated and not working in silos. The same is observed in the applicability of the economic theories as well. It is the combination of Keynesian thinking and the monetarist philosophy i.e., a mix of monetary and fiscal measures which has the capacity to bring back the economies out of the scares of recession.

That seems to the possible reason that, after series of regulatory initiatives, the Indian economy got four booster doses from the Government, last one being that of reduced Corporate tax rates, which we believe is a strong move signaling governments intent of being proactive in using fiscal tools to help economic revival of the country.