The US Dollar has been the global reserve currency ever since 1944 when the Bretton Woods Agreement was signed between the major nations of the world.

For the uninitiated, a global reserve currency is a foreign currency held in large quantities by central banks of other countries as foreign exchange reserves for international trade, investments and other transactions. Generally speaking, there has always been only one predominant global reserve currency at any point of time although several other satellite currencies have concomitantly had a considerably lesser role.

Reserve Currency Fortunes

Global reserve currencies have waxed and waned with the ups and downs of the geopolitical power of their issuers. Accordingly, this privileged position has been held in the past by the British Pound Sterling, Greek Drachma, Roman Denarius, Byzantine Solidus, Arab Dinar, French Franc, Venetian Ducat, Florentine Florin, Spanish Dollar, Dutch Guilder, etc. at various points in history. In general, the demise of global reserve currencies has been preceded by the issuers inability to effectively control their purchasing power mainly because the issuing government was unable to resist the temptation to debase the currency by unrestricted printing. Nowadays it is fashionable for such printing to be called “quantitative easing” so as not to offend the sensibilities of those who are sensitive. Ultimately, no currency of any kind, reserve or otherwise, has survived forever. There have been thousands of currencies in world history and the fact that not one of them has survived for lengthy periods of time should serve as a warning to financiers that the failure of any given currency is a certainty and not a probability. In other words, currencies are an illusion with an all too finite life.

However, global reserve currencies dance while the music is still playing, and as long as the illusion lasts, it bestows an exorbitant privilege upon its issuer. Its issuer can borrow at lower costs because other countries are forced to maintain reserves of its treasuries because of the need for an international reserve piggy bank to finance international trade. This artificially low cost of capital enables the issuer to browbeat its opponents with powerful military and trade sanctions which in turn strengthens its currency even further, thus creating a virtuous cycle for at least as long as the music plays. However, no global reserve currency is immune to the ultimate fate of any currency and must ultimately collapse because it will ultimately quantitatively ease itself out of existence.

Gold Pegs

Throughout world history gold has been a restraining influence on sultans and kings, emperors and tsars, presidents and prime ministers who would have printed currency like there was no tomorrow if not for the firm discipline of gold. It was JP Morgan who said, “Only gold is money. Everything else is credit”.

Traditionally, all global reserve currencies have generally been pegged to gold. This peg serves as a backstop against the issuers tendency to print more of the currency in an effort to boost spending and maintain the illusion of power. The US dollar is no exception to this rule. In 1944, the US dollar was pegged to gold and holders were free to exchange US dollars for gold at the rate of US$ 35 per ounce. But alas, the US was not immune to the great temptation of governments – the uncontrollable urge to spend. Thus it was that the US went to war with Korea and Vietnam in the 1950s and started to print more US dollars than the amount of gold in their reserves so that they could fund these military misadventures.

Of course, other countries are not suckers and this debasement of the US dollar inevitably led to increasing demands from world governments for the conversion of their US dollar reserves into gold until the US was forced into default on 15-Aug-1971 when President Nixon announced that US dollars could no longer be exchanged for gold at US$ 35 per ounce. Currency markets were closed for several days and then reopened under the so-called floating rate system where foreign exchange rates were determined by market equilibrium in currency markets. Thus the US dollar became a 100% fiat currency.

Petrodollar Party

It was the first time in world history that the global reserve currency was pegged to nothing except the full faith and credit of a particular government – in this case the US Government. Considering that the US Government had just defaulted, it was doubtful whether it had either the faith or the credit to continue as the global reserve currency. If anything the US dollar was actually pegged to the lack of faith and credit of the US Government.

Just three years later in 1974 the US Government and the King of Saudi Arabia, who was the world’s biggest crude oil supplier, signed an agreement by which Saudi Arabia would price its crude oil in US dollars and in return the US would install US military bases within Saudi Arabia and sell sophisticated weaponry to Saudi Arabia.

Even today the US maintains 5 military bases in the Islamic holy land of Saudi Arabia which are the cause of much heartache among Saudi Arabian citizens – 15 out of the 19 men who were involved in the World Trade Center attacks on September 11, 2001 in New York were Saudis. Even today Saudi Arabia is the world’s biggest importer of US military equipment.

Several other oil producing Middle Eastern nations followed suit and thus the US Dollar was pegged to crude oil – a commodity far more valuable than gold. The US Dollar had effectively obtained currency nirvana and slowly but surely everything began to be priced in US dollars and it had redeemed itself as the global reserve currency by piggybacking on Middle Eastern oil and insecurity.

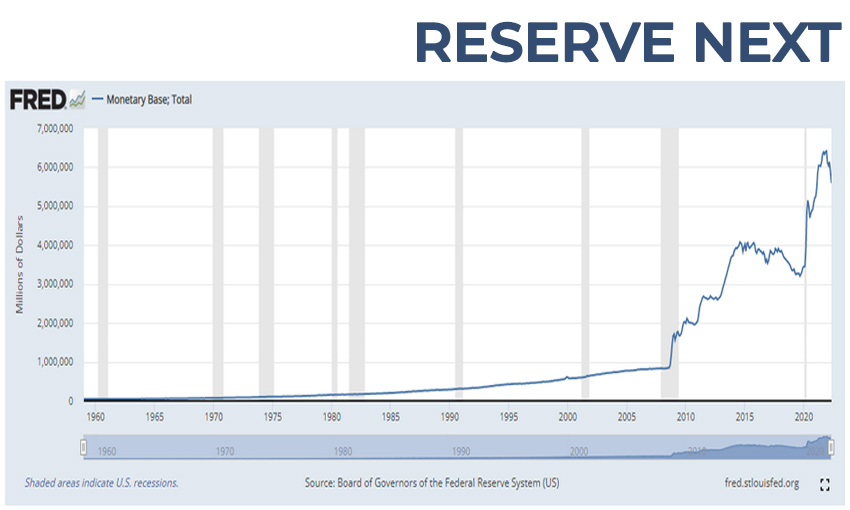

Quantitative Unease

Everything was chugging along smoothly until the US Dollar caught the printing disease all over again. The world of finance is filled with euphemisms because brutal frankness injures the delicate sensibilities of ruthless moneymen. Thus “Printing Money” is called “Quantitative Easing” or “QE” for short, in financial circles. A quick look at the above chart showing the US Monetary Base since 1960 will convince anybody about the need for such a euphemism.

One can argue that the US has been printing dollars with reckless abandon because of the Great Recession in 2008 and the Covid Pandemic in 2020. However, the fact is that only less than US$ 1t had ever been printed until 2008 since its invention more than 200 years ago but is close to US$ 6t these days. In other words, over 80% of US dollars did not exist before 2008, i.e., 5 out of every 6 US dollars has been printed in the past 14 years.

Monetary Phenomena

It does not require a Nobel Prize winning economist to interpret the above chart but it was Milton Friedman who emphatically observed that inflation is always and everywhere a monetary phenomenon. In other words, if you print money, inflation follows. But with no gold peg to provide a restraining hand, the US Government is firmly convinced that the rest of the world will have no choice but to fund its deficit because there is no alternative.

While uncontrolled money printing brings inflation to the country issuing the currency, the US Dollar has also brought raging inflation to the rest of the world because it is the global reserve currency and the price of everything is quoted in US dollars. The price of almost every commodity has risen without any appreciable change in supply. It is not the value of these commodities that has risen, it is in fact the value of the US dollar that has diminished. Commodity price inflation is a monetary phenomenon.

The Russians Gambit

Those with hammers look for nails – so governments who issue global reserve currencies look to sanction others. The US Government has never hesitated to sanction anybody and Russia was right in their sights after the start of the Russia-Ukraine war.

Unfortunately, the Russians are excellent chess players and they simply pegged the Russian Ruble to gold instead of the US Dollar to stabilize their currency. The Russians now demand payment either in gold or in Ruble from “unfriendly” countries wanting to trade with them and they can because they are world leading suppliers for many commodities including oil, gas, precious metals and food grains.

Reserve Next

John Maynard Keynes at Bretton Woods in 1944 had suggested a new supra national global reserve currency that he called the Bancor which would be based on a basket of several national currencies. So opposition to having a particular country’s currency as the global reserve currency started from the very beginning and that too by one of the world’s greatest economists.

The first tsunami that shook the US Dollar to its foundations was the 1971 Nixon Shock when the US defaulted on its obligations to exchange US Dollars for gold at the rate of US$35 per ounce. In 1969, the International Monetary Fund (IMF) anticipated the upcoming US default and had created the Special Drawing Rights (SDR) constituted of a basket of several national currencies as an alternative global reserve currency issued by the IMF.

In 2009, in the midst of the Great Recession, Zhou Xiaochuan, Governor of the Peoples Bank of China, stated that the 2008 financial crisis was exacerbated by the US Dollar based global reserve currency system which needed to be replaced by an SDR based system if the world was serious about tackling the flaws of having a national currency as the global reserve currency. He was referring to the famous Triffin dilemma faced by a country issuing the global reserve currency who must then target domestic monetary policy goals while simultaneously meeting the demand for the reserve currency by other countries – an impossible task. An undue concentration of sovereign reserves in any one currency brings about undesirable outcomes.

In 2020, Kristalina Georgieva, IMF Managing Director urged a reworking of the global reserve currency system because of the destabilizing effect of the expansion of central bank balance sheets totaling up to US$ 7.5t in response to Covid. She urged the world to seize this new Bretton Woods moment.

The world needs a new global reserve system that is fair and equitable to all countries and that will be achieved only with the arrival of the next reserve currency.