Reality in real estate gains

Before dreaming more, let us see whether Rohan is liable to pay any tax on this gain of 15 lakhs. Yes, the gains from real estate sale are liable for taxation under capital gain. Let us see how the taxation works here. The gains from such deals are divided into:

- Short term capital gain (STCG)– if the asset is held for less than 36 months

- Long term capital gain (LTCG) – if the asset is held for more than 36 months

Now, let us see how these gains are taxed.

Taxation on short term capital gains:

In the case of short term capital gain, you will be taxed as per your tax slab rate. If you are in the 30% tax slab, you are liable to pay 30% on the gains. Rohan is in 30% tax slab and he has to pay 30% of his gain as tax. After paying 4.5 lakhs as tax, his net gain is only 10.50 lakhs. This translates into a return of around 16% for the last 2 years, not that high. Even equity mutual funds have delivered similar return in the same period.

If you are selling a property within 3 years, be prepared to pay huge tax. You cannot avoid this tax.

Taxation on long term capital gains

The taxation on long term capital gain is more liberal. Such gains will be taxed at 20% after indexation benefits. Indexation is a mechanism to adjust the cost of investment for the inflation. Let me explain what indexation is.

Indexation – way for reducing tax

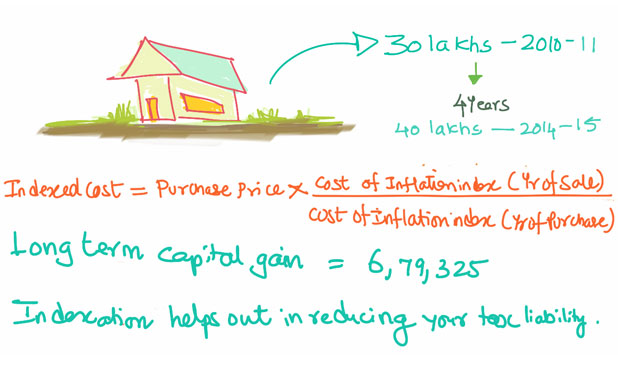

Every year, the government will notify the Cost of Inflation Index based on the prevailing inflation rate in the country. The cost of inflation index value for 1981-82 is 100. The index value was 711 for financial year 2010-11 and 1024 for 2014-15. Let us see how indexation helps in reducing tax.

Atul purchased a flat in 2010-11 for 30 lakhs and sold it in 2014-15 for 50 lakhs. The asset was held for 4 years and the gain will be treated as long term capital gain.

In this case, the indexed cost = 30 lakhs x 1024/711 = 43, 20,675.

{kind=link}

Long term capital gain = Sale price – indexed cost

The long term capital gain = 50, 00,000 – 43, 20, 675 = 6, 79,325. His tax liability will be 20% on this gain of 6, 79,325 and it works out to 1, 35,865. Indexation helps you in reducing your tax liability.

While calculating the LTCG, you can deduct any expenses incurred for brokerage on sale. The amount spend on improvement of the property can also be deducted after indexing such cost.

Options to reduce the Long term capital gain tax

You can reduce your tax liability on LTCG by adopting certain permissible investments/savings.

Tax savings under Section 54

You can reduce your tax liability from LTCG if you are investing the capital gain in a residential property. Such investment should be done before one year of this sale or within 2 years from the sale. In the above example Atul sold his flat on 10th April 2014. He can save tax if he invest the gain of 6, 79,325 in another residential property during the period from 10th April 2013 to 9th April 2016. He can construct a house using this gain within 3 years from 10th April 2014 and save tax. The investment is limited to only one property as per the last year budget.

Capital Gains Account Scheme

Though the rules give you 3 years time to invest the capital gains in another property, you cannot keep the amount with you for these 3 years after the sale. If you are not utilising the gains for buying or constructing the property before the due date of filing of returns of that year, you have to pay tax on such gains. To avoid such situation government has introduced a scheme called Capital Gains Account Scheme. You can invest the unutilized amount of capital gain in that account before the due date of filing IT return and avoid paying tax. As and when you require investing in the new property, you can withdraw from this account. Any unutilized amount after 3 years will be treated as long term capital gain of that year and will be taxed.

Tax savings under Section 54EC

If you are not interested in investing in another property, you can still save tax on LTCG. You can do this by investing the LTCG in specified bonds for a period of 3 years. Such bonds are issued by Rural Electrification Corporation (REC) and National Highways Authority of India (NHAI). These bonds are for 3 years and carries interest rate of 6%. You have to make such investment within 6 months from the date of sale and the maximum permitted amount is 50 lakhs.

Plan your real estate investments carefully

When you are going for the next real estate investment, think twice. Ensure that your gains are not eaten by the tax man.

Real estate should be part of your portfolio – not the entire portfolio.

Create a portfolio which is diversified. An ideal portfolio should have a mix of equity, Debt, Gold and Real estate. If you are over exposed in any asset class now, try to balance it by adding more assets in other asset classes.