Any man’s death diminishes me,

Any man’s death diminishes me,Because I am involved in mankind,

And therefore never send to know for whom the bell tolls;

It tolls for thee.

These poignant words by the English poet and priest John Donne (1572-1631) have inspired many through the centuries, including Ernest Hemingway to write his celebrated novel set in the Spanish Civil War ‘For whom the bell tolls’. Financial markets, of course, have no moral compass but it still came as a shock as to how quick they have been to discount the potential of the Wuhan Coronavirus (COVID-19) pandemic to disrupt and seriously harm the global economy. They may yet have second thoughts as the strength of the global economy is brutally tested.

Any attempt to quantify either the direct or indirect impact Coronavirus is hampered by almost universal scepticism over the official data in China. So far there has been an official cover up and now it seems that the authorities have departed from the World Health Organisation’s classification of ‘confirmed cases’. Doubts were further fuelled by the publication on a Tencent website of ‘official’ data that was rapidly replaced with much lower official numbers.

Also being questioned is the source’s being as simple as a food market in Wuhan. More sinister is controversial speculation that the Coronavirus had been modified for future biowarfare and had somehow been released from a laboratory in Wuhan.

Apparently, the virus is not as lethal as many other mass infections, including ‘ordinary’ influenza, but it is more contagious with the potential to create just as much human misery as the worst pandemics.

There is an ongoing debate about the length of the incubation period but the decisive stage of the infection itself is reckoned to be in the second week and sufferers either recover or die in the third week. The most vulnerable are asthmatics, smokers and the aged but over 1,700 doctors in China are reported to be infected. Professor Gabriel Leung, the chair of public health medicine at Hong Kong University (a veteran from the SARS pandemic), has estimated that in its current form the Coronavirus has an ‘attack rate’ is 2.5 transmissions by each infected individual.

The resulting numbers of confirmed cases and deaths (currently estimated at a rate around 1%) is simply terrifying but Professor Leung also believes the virus could mutate to become less pernicious. Amidst so much human misery, it is the threat of contagion that is likely to inflict the most economic damage.

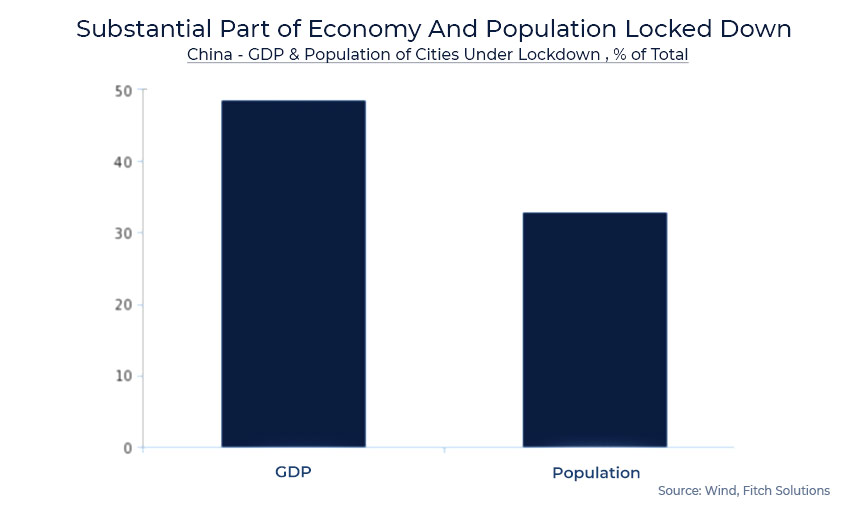

Figure 2: Contagion control: Too much too late?

China and the global economy’s biggest test yet

Reuters have reported that President Xi is now concerned that the belated measures to limit contagion, including travel bans and enforcing strict quarantine (Figure 1), are too drastic and is ordering businesses, most if not all of which have effectively been shut down since the start of the New Year Holiday in the last week of January, to get back to work. This is despite the official view that the pandemic will peak in March and is a lot easier said than done, not least because of a chronic shortage of facemasks.

Figure 2 shows that Mr Xi is surely right to be concerned about the damage to China’s economy with a third of the national population and almost half of GDP locked down. Various brave forecasters are already suggesting that it will be mainly confined to the current quarter, resulting in full year growth of ‘only’ around 0.5% lower than in 2019. Such forecasts appear to gloss over the fact that even the Government had admitted before the advent of Coronavirus, COVID-19 that the rate of GDP growth was slowing, which has been confirmed in a run of tepid (some more than others!) Purchasing Manager Surveys. The travel and quarantine restrictions are bound to hit Consumption and business in the tourist (the China Grand Prix is under threat), catering and recreation sectors will be lost forever. In the Province of Hubei and Wuhan City itself there are reports of shortages of food and other retail supplies.The Government has encouraged the development of the Services Sector as a whole and it now accounts for over half of GDP.

Importers and retailers, especially of upmarket cars and other luxury products, are being hit by collapsing demand and under-staffed ports and other entrepots. Corporate cash flows are under pressure , wages are being lost and many workers will no longer have jobs to return too.

The Manufacturing Sector will, of course, be able to catch up but there could well be short-term capacity constraints and longer-term business may have been lost to competitors outside China or to re-sourcing to home countries in North America, Europe and Japan. The US-China trade dispute had already caused multinational corporations to investigate setting up parallel supply chains to avoid tariffs and possibly as a kind of political risk insurance. This is unlikely to be easy to implement quickly and Fiat Chrysler, Ford, Jaguar and JCB are only frontrunners in their posting warnings. Importers of textiles, computer and other electronic equipment, pharmaceuticals and non-metallic minerals from China are especially exposed. Somewhat piquantly, the US sources almost all surgical masks and most of its antibiotics from China, together with syringes and surgical gloves. Chinese tourists are famously free-spending on their travels and will be especially missed in the US, Japan, UK and Italy. Global trade and business fairs are being postponed or scaled back because of

attendee withdrawals.

The cancellation of scheduled airline flights and the evacuation of foreign nationals are adding drama to the growing sense of isolation. Foreign Direct Investment can be expected to slow at least for a while despite the lure of access to 1.4bn Chinese consumers.

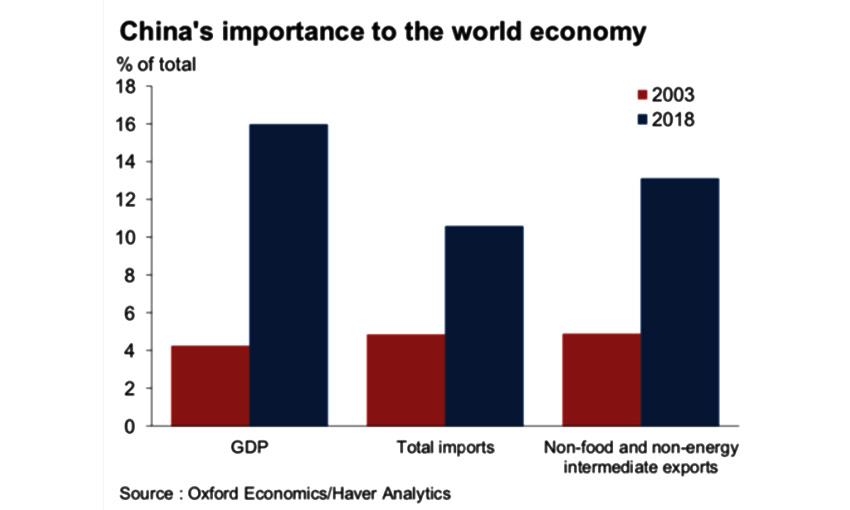

Figure 3: As China’s economy sneezes, will the world economy catch cold ?

Figure 3 highlights just how much more greater has become China’s share of global output and even more so of global trade than in 2003 at the time of the SARS epidemic. Growth forecasts for both China’s imports and exports are being revised lower together with consequent reductions to Q1 GDP growth elsewhere. The most affected in relative terms will be inevitably be the geographically nearest economies, notably South Korea, Australia, Indonesia, Japan, Taiwan and Kazakhstan but in absolute terms the US, Germany and India will also take major hits. It comes as no surprise that the central banks of Thailand, Philippines, Russia and Brazil have been quick to cut official interest rates.

Unless the pandemic really does peak in March there will be much greater disruptions and emergency corporate and governmental measures. The global economy has never really recovered from the Great Financial Crisis and will struggle with a major new test of its resilience.