So that U-turn was fast, even for the legendarily cyclical trucking business.

The chart below shows the percent change of Class-8 truck orders for each month compared to the same month a year earlier, which eliminates the effects of seasonality. The year-over-year plunges in December and January are on par with happened during the last transportation recession (data via transportation data provider FTR):

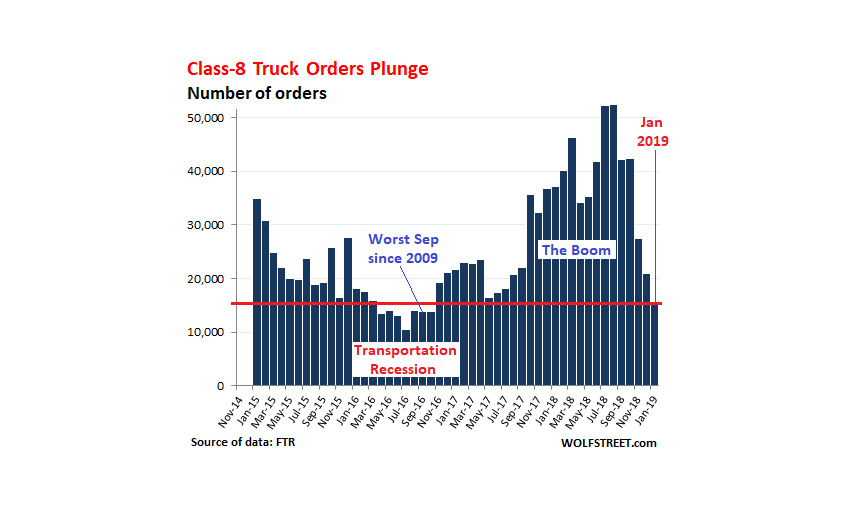

In the chart above, also note the blistering boom in orders in 2017 and 2018, when demand for transportation services soared, and trucking companies that found themselves short on equipment went on an ordering binge, trying to be the first to get their orders into the system. This historic explosion in orders led to a record backlog for truck makers and their suppliers.

Then, in this viciously cyclical industry, the cycle progressed to the next phase, with demand for transportation services returning to normal-ish levels, even as capacity was rising, and truckers slashed their orders for new equipment.

The chart below of the number of orders for Class-8 trucks every month shows how far these orders have dropped, from over 50,000 each in July and August to 15,642 in January:

It was, however, a predictable U-Turn. Following the August 2018 data, I asked at the time, When will the biggest-ever boom end? And I cautioned that this boom could not go on like this. A month later, with the September data, I provided the answer: Signs that the Trucking Boom Has Peaked. And I added in the subtitle, “This is why the trucking business is so cyclical – and you can see it coming.”

So what does this mean?

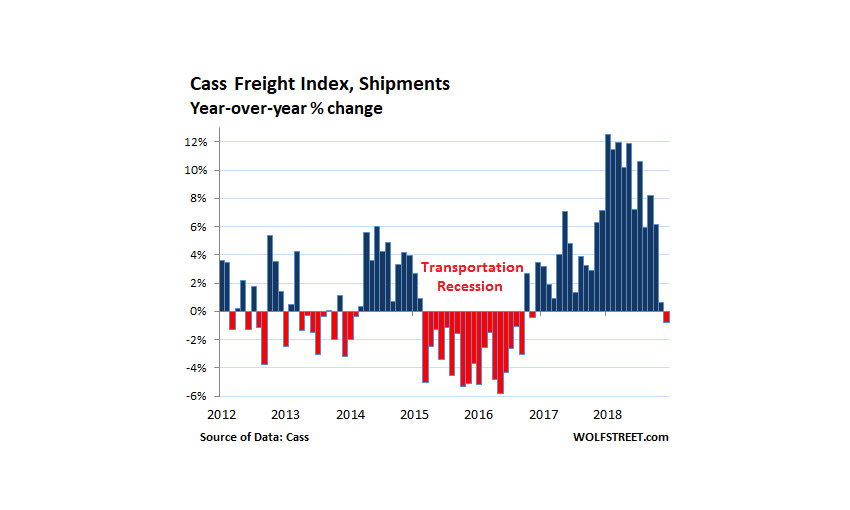

We have already seen that freight shipment volume across all modes of transportation – truck, rail, air, and barge – in December had declined a tad from a year earlier, according to the Cass Freight Index. The index covers shipments of merchandise for the consumer and industrial economy but does not include bulk commodities, such as grains or chemicals. It was the first year-over-year decline since the transportation recession of 2015 and 2016 — and trucking companies have seen this coming for months:

Over the past 12 months through January 2019, truckers ordered about 450,000 Class-8 trucks, while US truck makers have an annual capacity of about 320,000 trucks, which averages out to about 26,500 per month. So the phenomenal spike in orders in early and mid-2018 led to a historic backlog that truck makers are still working through. There have been some cancellations, and the backlog is shrinking, but it still extends well into this year.

The trucking business is a barometer of, and dependent on, the goods-based economy. In late 2017 through the summer of 2018, demand for transportation services, such as shipping by truck, surged under the simultaneous impact of a strong goods-based economy led by red-hot e-commerce; a buildup of inventories; pandemic front-running of potential tariffs, a resurgence of drilling activity in the oil patch that required equipment and supplies to be trucked in, etc. Freight rates spiked. Squeezed shippers wheezed in their earnings reports about these spiking transportation costs, while truckers were on Cloud-9 and ordered new trucks to meet the demand, and truck manufacturers were swamped with orders.

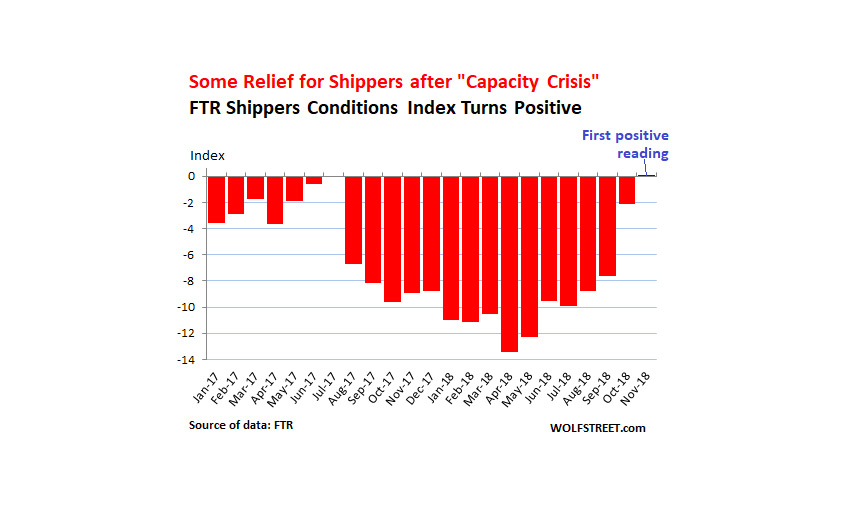

These shippers that had struggled with a “capacity crisis” in mid-2018 are now seeing signs of relief. This is reflected in the FTR Shippers Conditions Index, which combines four major conditions in the full-load market — freight demand, freight rates, fleet capacity, and fuel price — into an index. “A positive score represents good, optimistic conditions. A negative score represents bad, pessimistic conditions,” FTR explains. The most recent update, released January 24, is for shipments in November. The index was deeply negative as surging costs hit home. But in November, the index turned positive just a tad, the highest reading since August 2016:

“Conditions have improved noticeably for shippers in the last few months,” said Todd Tranausky, FTR VP of rail and intermodal. “The prospect of sustained lower fuel prices, increasing capacity in the truck and rail sectors, and the first signs of a turn in rail service raise the prospect of a much better 2019 than shippers expected during much of 2018.”

Because there are always two sides to everything: The historic boom for the trucking industry was a nightmare for shippers; and a transportation recession, dogged by excess capacity, always feels like Cloud-9 for shippers.

Shipment falls but freight rates remain red hot. Read... Boom Fizzles: Shipments Fall for 1st Time Since Transportation Recession